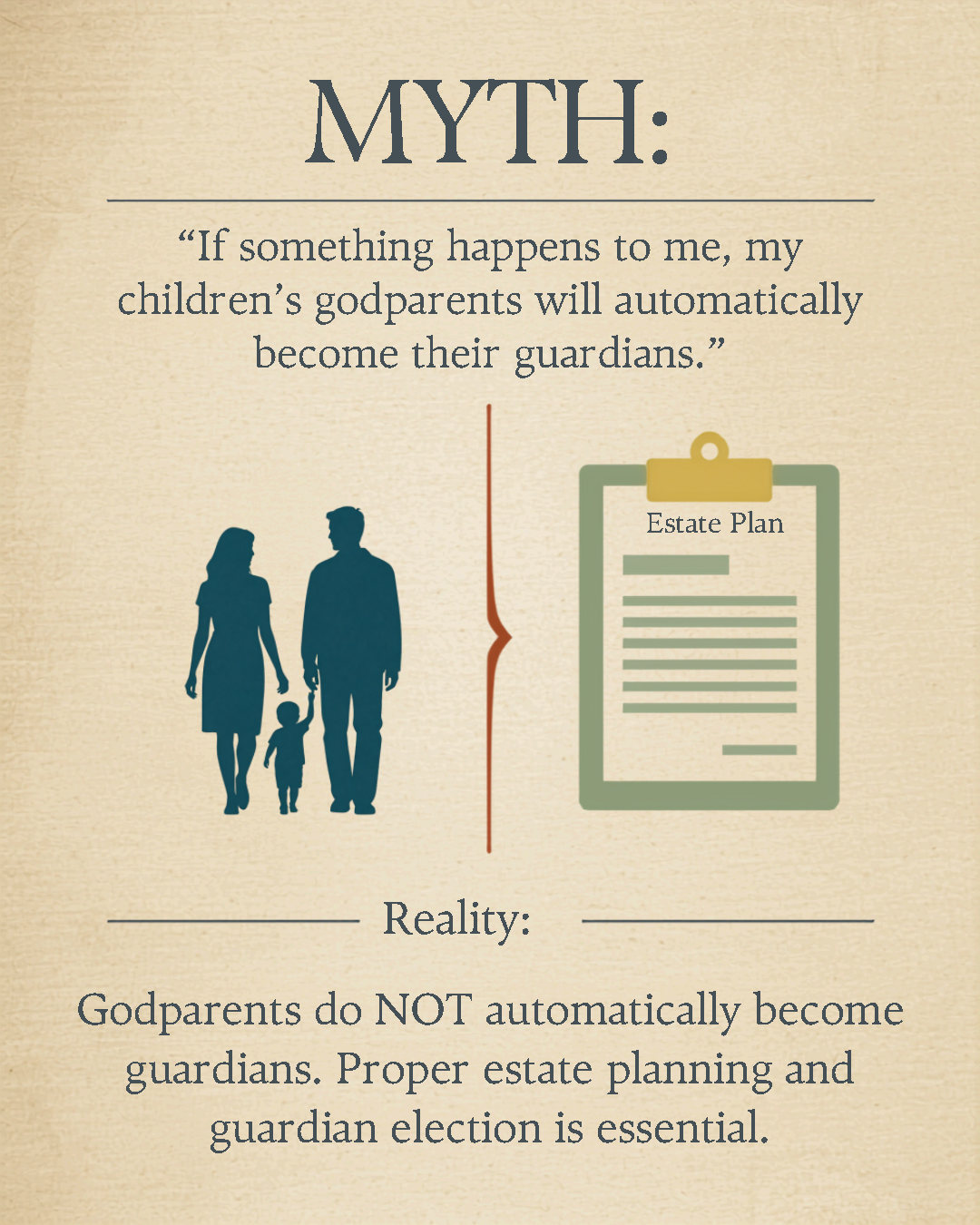

Myth: “Leave your estranged relatives $1 so they can’t contest your will.”

A common belief is that designating any portion of your estate to an estranged relative will legally prevent them from challenging your will. In reality, leaving someone anything in your will generally makes them an “interested party” in the eyes of the court, meaning they must be formally notified of the probate proceedings. This can inadvertently involve a disgruntled relative in your estate administration process, potentially leading to drama and confusion.

If your intention is to exclude someone from both inheriting any of your estate and from challenging your will, a carefully drafted disinheritance clause is, in most cases, the better approach. It clearly documents your wishes and helps avoid questions about whether the omission was accidental.

Disinheritance clauses aren’t just for estranged family members, either. They can also simplify estate administration in amicable situations as well, and help explain unequal distributions among family members. For example, a parent may have already provided extensive financial support or established separate planning—outside of a will or trust—for a child with special needs, making it appropriate for another child to inherit the estate. A thoughtfully-drafted disinheritance clause can clarify the reason for doing so. In such a case, the clause may include a phrase directed towards the disinherited child to show that the testator has made the decision “not for any lack of love or affection, but for reasons known to them.” Even if everyone agrees on who should inherit, clearly stating your intentions in your will can help make the probate process smoother.

Every family situation is different, which is why thoughtful estate planning is crucial. A properly drafted will can help ensure your wishes are carried out while minimizing unnecessary complications for your loved ones.

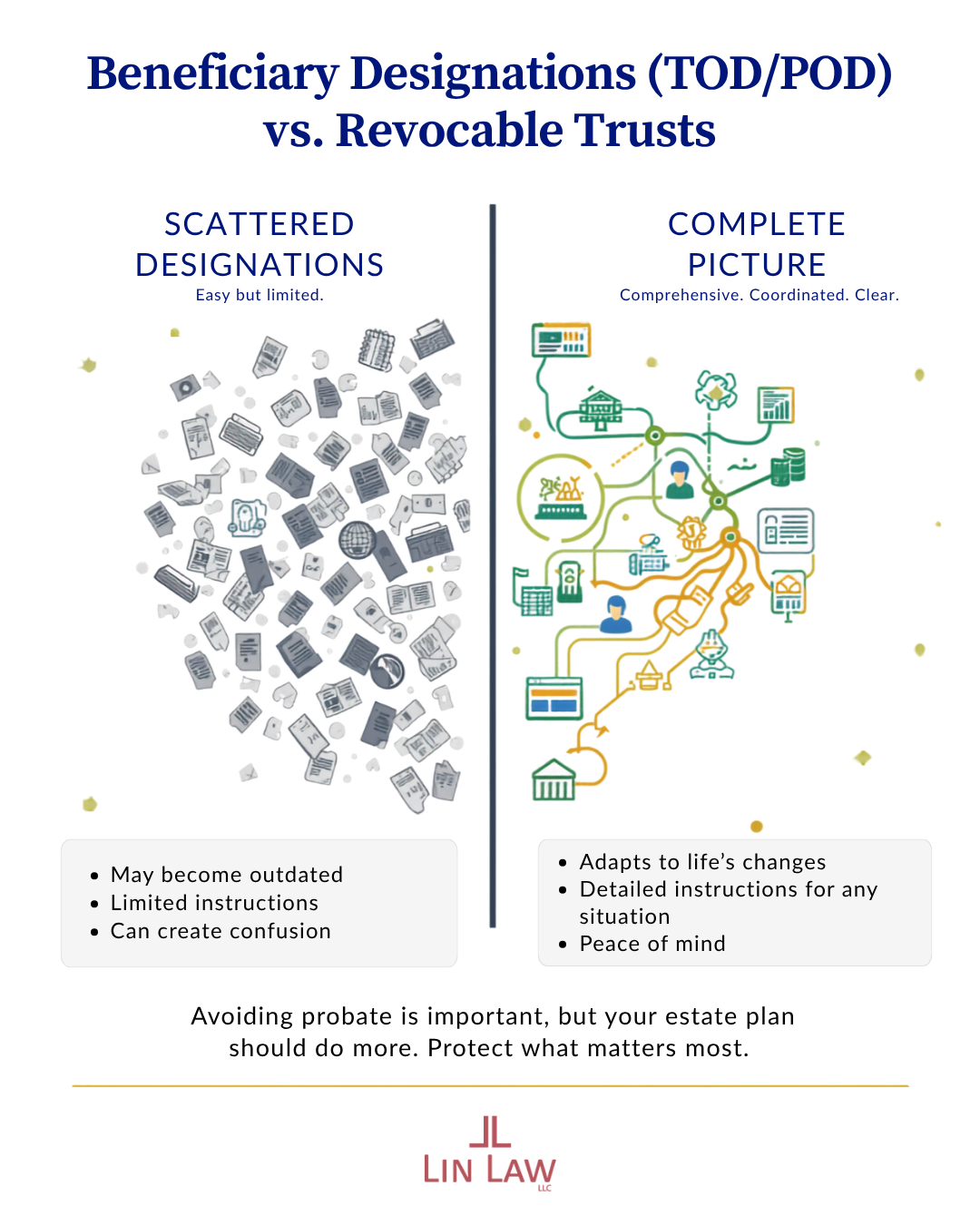

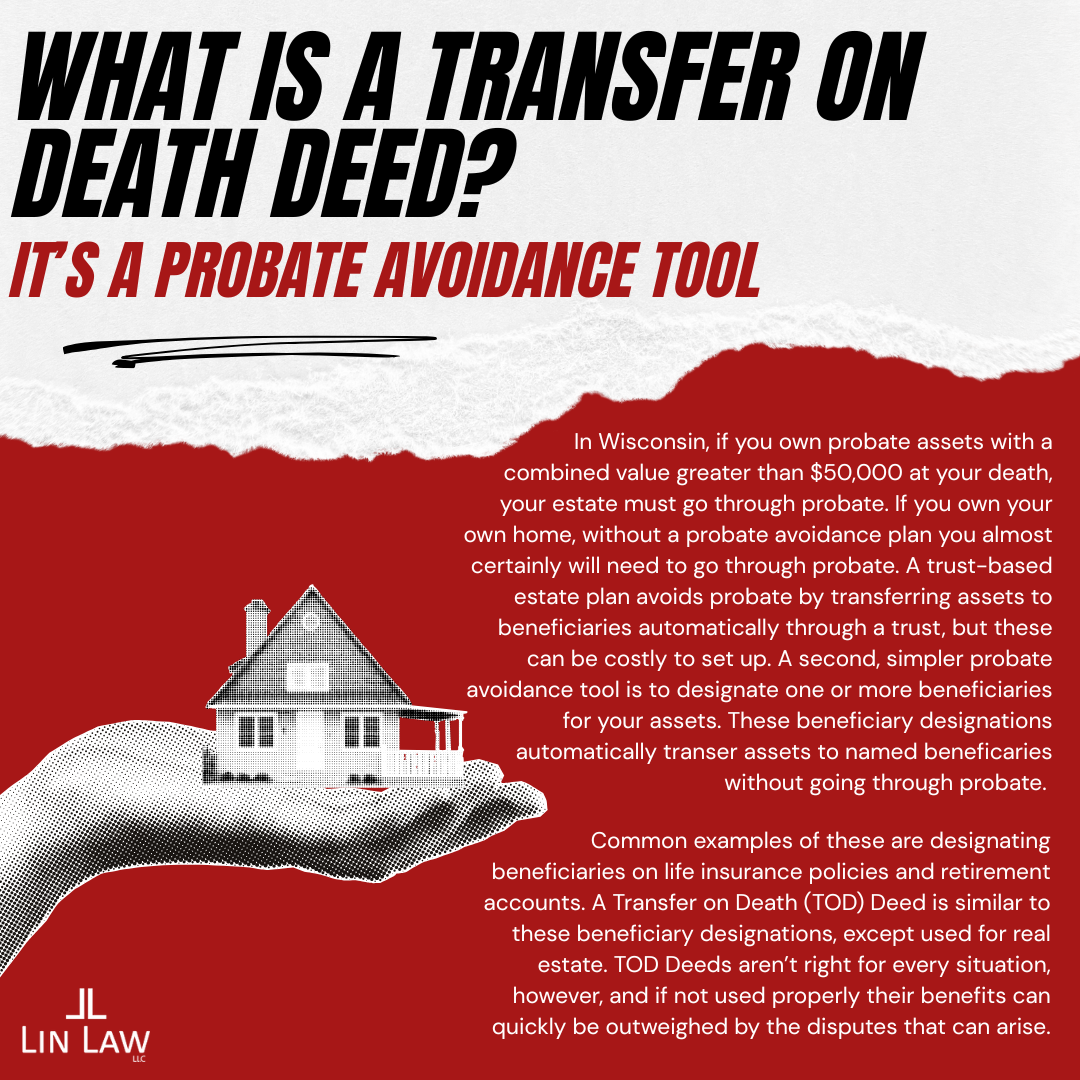

One of the most common misconceptions about estate planning is that adding beneficiary designations to your financial accounts will be enough to both avoid probate and have a comprehensive estate plan. However, while transfer-on-death (TOD) and payable-on-death (POD) designations can help pass assets directly to your heirs without probate, a clearly structured estate plan focuses on more efficiently managing assets and their distribution, since it takes into account unforeseen life changes that a TOD or POD designation does not account for. Avoiding probate alone should not be the only goal with respect to a complete estate plan.

One of the most common misconceptions about estate planning is that adding beneficiary designations to your financial accounts will be enough to both avoid probate and have a comprehensive estate plan. However, while transfer-on-death (TOD) and payable-on-death (POD) designations can help pass assets directly to your heirs without probate, a clearly structured estate plan focuses on more efficiently managing assets and their distribution, since it takes into account unforeseen life changes that a TOD or POD designation does not account for. Avoiding probate alone should not be the only goal with respect to a complete estate plan.

Persons involved in real estate closings and settlements are now required to report on certain transfers that the Treasury Department deems high risk for illicit financial activity. Specifically, non-financed transfers of residential real property to legal entities or trusts. The rule aims to in-crease transparency in real estate transactions and help prevent the use of anonymous entities to conceal illicit funds.

Persons involved in real estate closings and settlements are now required to report on certain transfers that the Treasury Department deems high risk for illicit financial activity. Specifically, non-financed transfers of residential real property to legal entities or trusts. The rule aims to in-crease transparency in real estate transactions and help prevent the use of anonymous entities to conceal illicit funds.

Did you know that Wisconsin is one of just nine states with marital (community) property laws? Wisconsin joined the small number of states with this treatment of marital property by enacting the Wisconsin Marital Property Act in 1986. Under Wisconsin’s marital property law, nearly all assets and debts acquired during a marriage are considered to be owned equally by both spouses, regardless of whose name is on the paycheck or whose name is on the title. The law is based on the principle that “a sound marriage is a partnership of equals,” recognizing the value of both financial and non-financial contributions to the relationship.

Did you know that Wisconsin is one of just nine states with marital (community) property laws? Wisconsin joined the small number of states with this treatment of marital property by enacting the Wisconsin Marital Property Act in 1986. Under Wisconsin’s marital property law, nearly all assets and debts acquired during a marriage are considered to be owned equally by both spouses, regardless of whose name is on the paycheck or whose name is on the title. The law is based on the principle that “a sound marriage is a partnership of equals,” recognizing the value of both financial and non-financial contributions to the relationship.

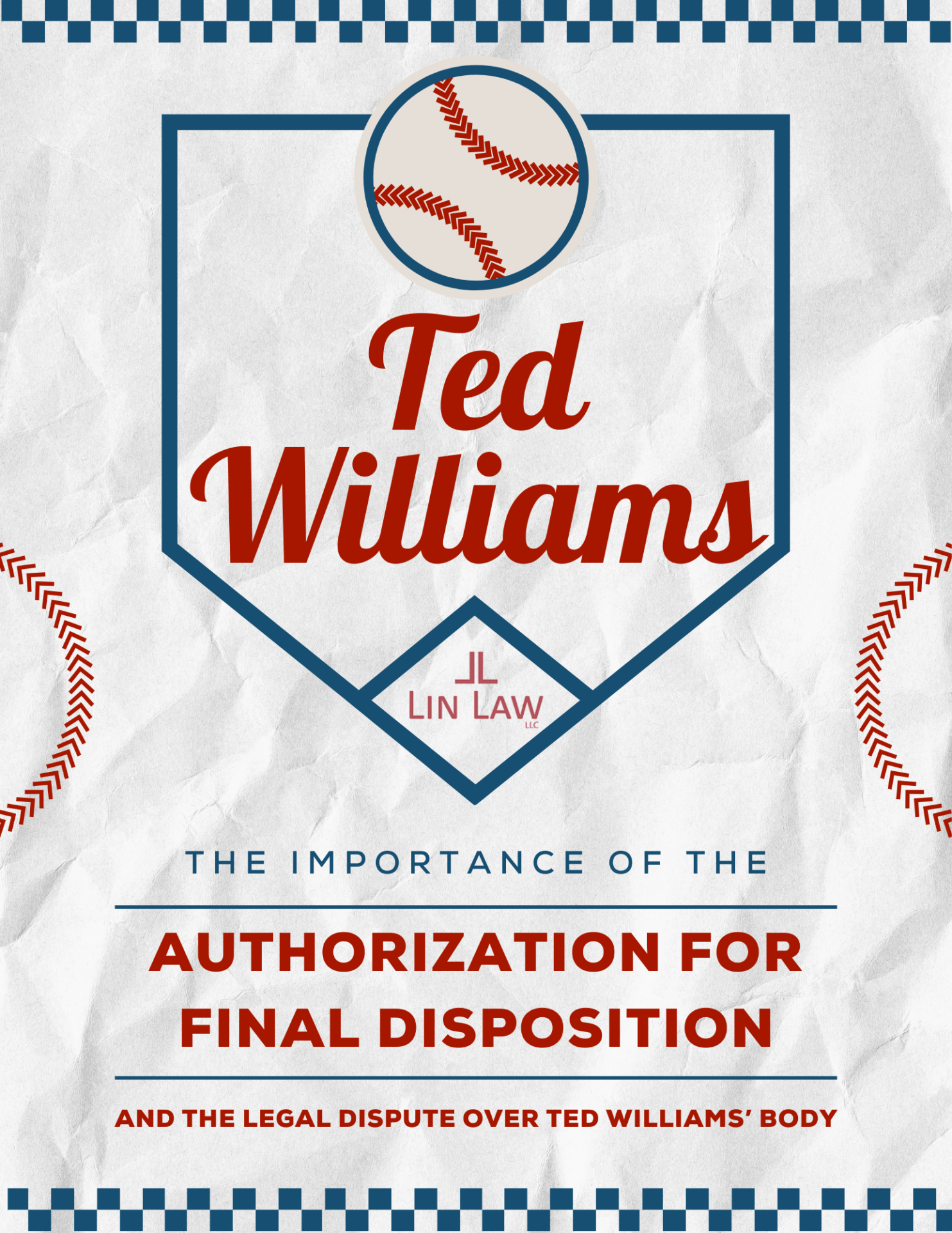

Even the best hitters can’t plan for every curveball life throws – but a strong estate plan, drafted by an experienced attorney familiar with your unique circumstances and goals, can bring your batting average up to all-star levels.

After Ted Williams passed away, confusion quickly ensued when two of his children presented a handwritten note expressing Mr. Williams’ desire that his body be cryogenically frozen. The problem? Mr. Williams’ will stated his wish to be cremated and have his ashes scattered over the ocean off the coast of Florida. The litigation that followed left Mr. Williams’ body frozen in controversy – like a batter getting thrown a 12-6 curveball.

Disputes like these can be avoided by properly documenting your wishes and by ensuring consistency across your estate planning documents. Wisconsin permits individuals to create Authorizations for Final Disposition – a special document that designates who will make burial or cremation decisions, and in which you may specify any specific funeral/celebration of life and burial arrangements.

At Lin Law LLC, we help families make sure their wishes are honored, their loved ones are protected, and their legacy is preserved.