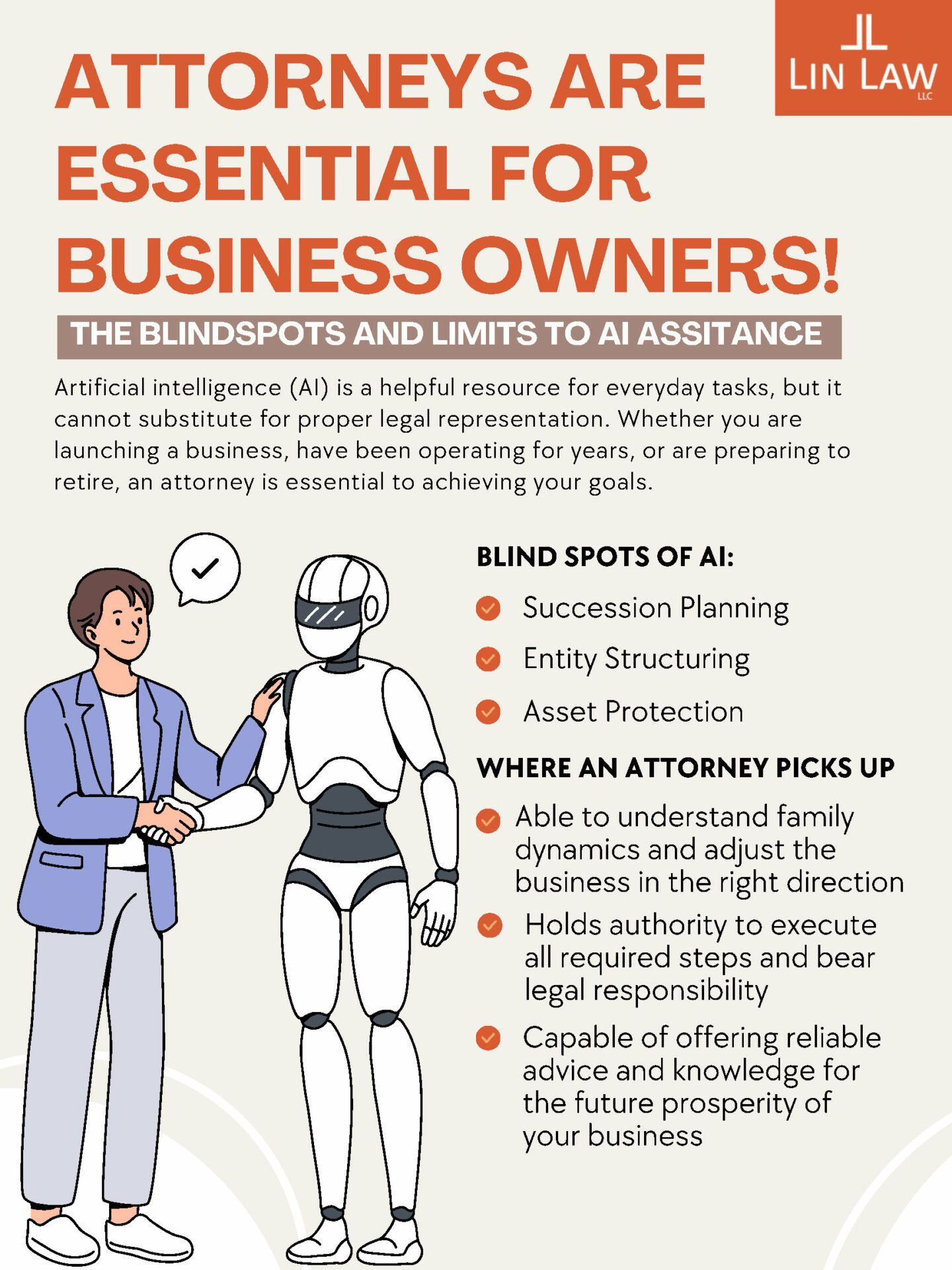

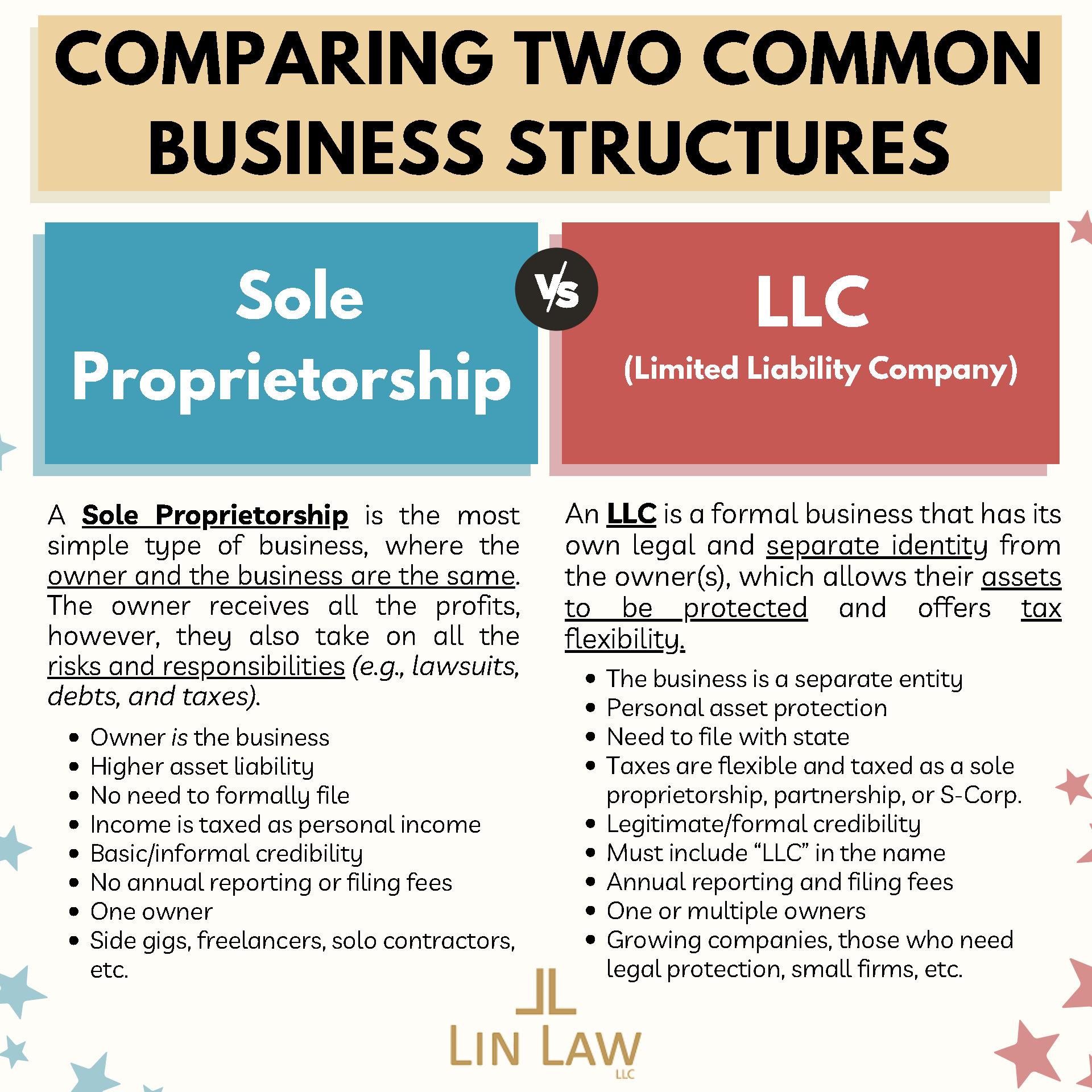

Artificial intelligence (AI) is a helpful resource for everyday tasks, but it cannot substitute for proper legal representation. Whether you are

launching a business, have been operating for years, or are preparing to retire, an attorney is essential to achieving your goals.

An attorney provides comprehensive protection and support, offering tailored advice to guide your business decisions toward long-term success. They spot blind spots AI can’t see:

- Succession Planning: Attorneys understand family dynamics and how personal relationships can affect professional goals. AI, by contrast,

offers a one-size-fits-all approach and cannot balance emotional or personal reasoning. - Entity Structuring: Attorneys create, maintain, restructure, and update entities, such as, drafting operating agreements, recording deeds, transferring ownership, handling trademarks, and managing asset sales or mergers. AI lacks the legal judgment to interpret overlapping statutes and has no fiduciary accountability or notary

- Asset Protection: Attorneys know state-specific asset-protection. They guide clients through rules like the Corporate Transparency Act and BOI filings and advise on tax-efficient strategies. AI may misapply these rules, potentially leading to costly missteps, or even allegations of fraud.

Avoid trouble and don’t risk your legacy. Attorneys are critical to business success:

- They personalize succession plans by navigating family dynamics and deploying tools like buy-sell agreements, trust management, and gradual ownership transfers; nuances AI cannot weigh.

- They ensure your business and estate are legally sound, executing all technical steps and administrative requirements. Attorneys bear legal

responsibility for your documents; AI software does not. - They offer reliable advice on how changing laws, such as, federalestate-tax exemptions or marital-property statutes, could affect your

plans and how to adapt for future success.

AI is great for quick answers to simple questions, but your business is worth more. Your life’s work deserves the detail and accountability only a qualified attorney can provide. An attorney delivers situation-specific guidance and proudly carries the responsibility of protecting your estate so it stands strong for generations; something AI simply cannot do.