Have you ever wondered what happens if you die without a valid estate plan? In legal terms, dying without a plan in place is called intestacy. Each state has its own set of intestacy laws that determine who inherits your assets. While intestate rules may vary slightly from state to state, they are intended to mirror what most people would want based on given family circumstances.

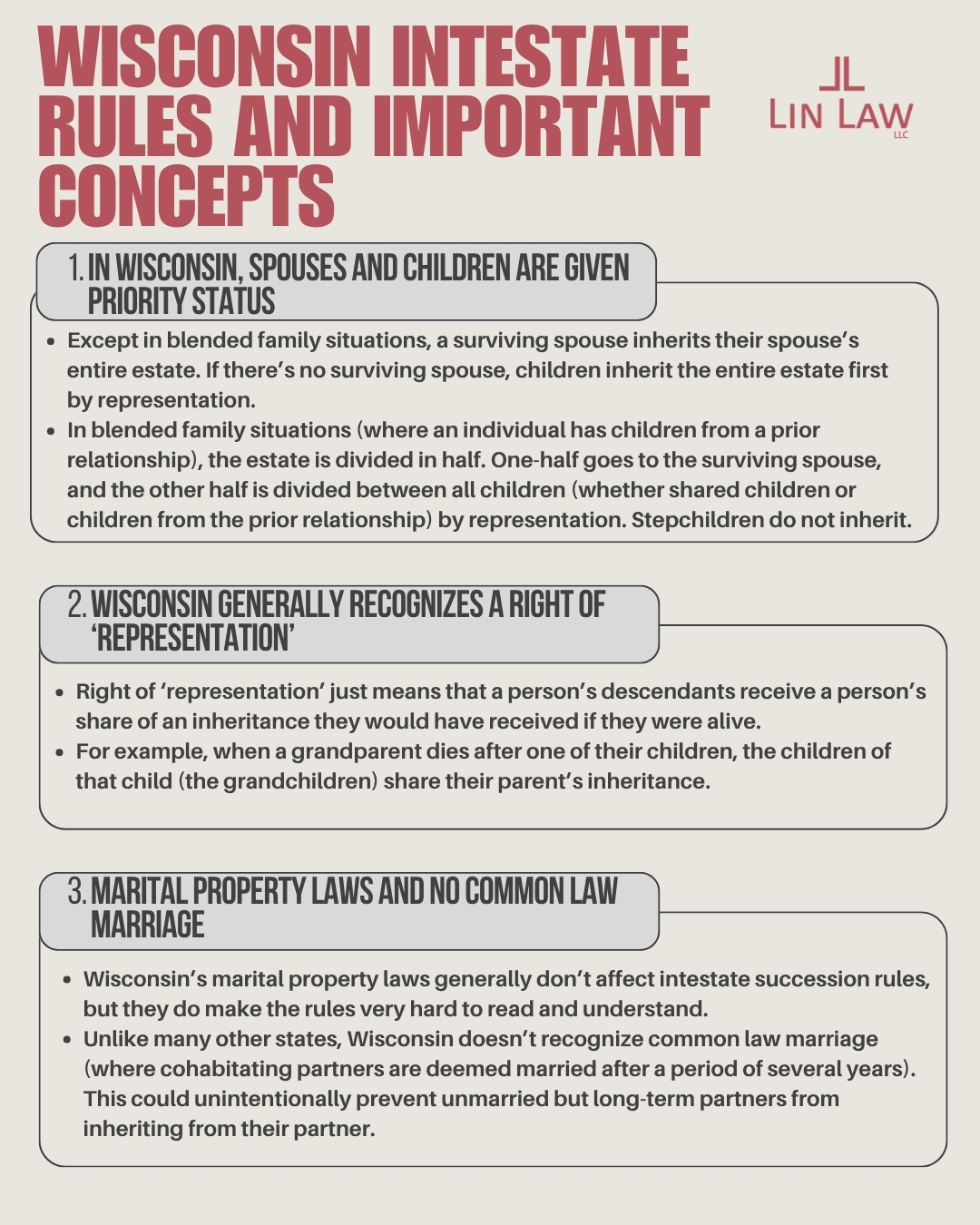

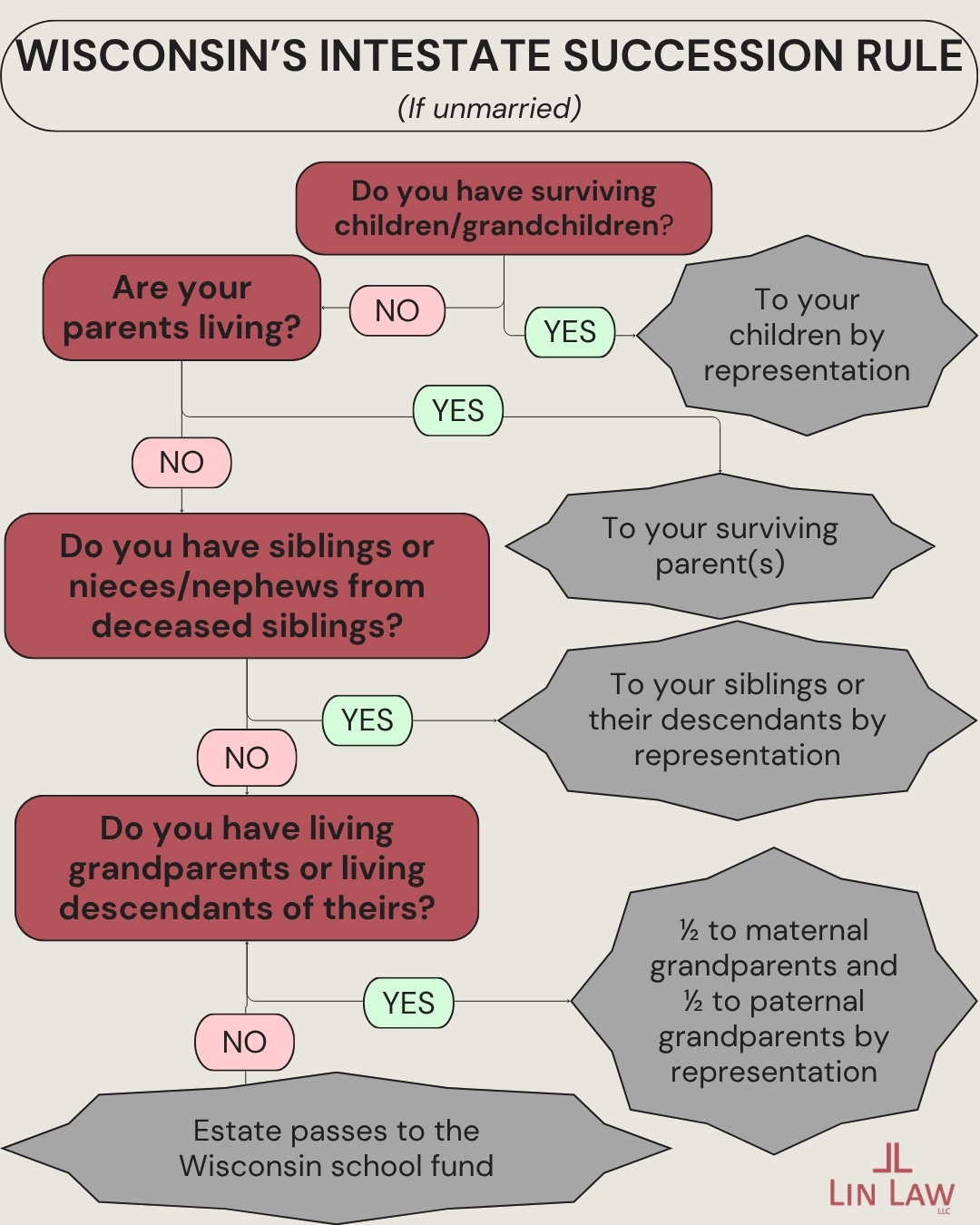

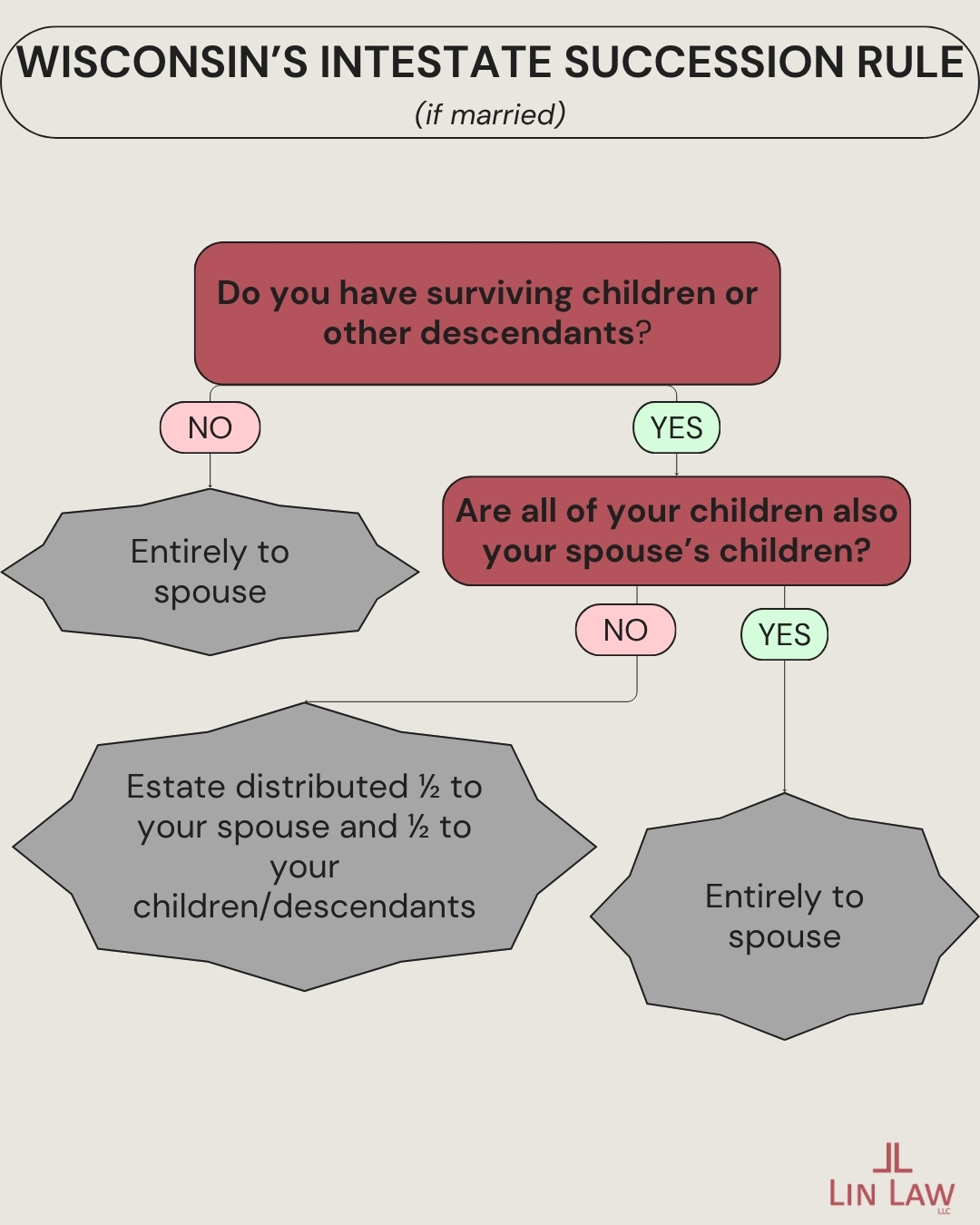

In Wisconsin, your spouse and children have priority status. If you are married and have no children, or if all of your children are shared with your spouse, your spouse inherits your entire estate. If you’re married but have children that aren’t shared with your spouse, then your spouse receives half your estate while your children share the other half equally by right of representation. If you’re unmarried but have children, your children inherit your entire estate equally by right of representation. If you’re unmarried with no children, then your next of kin inherit your estate.

Right of representation just means that a deceased person’s descendants share equally in the share that would have gone to that person had they been alive. For example, if your child dies before you but has surviving children of their own, then your child’s share is split equally between their children (your grandchildren).

It’s not uncommon to have different preferences than what “most” people would want, though. Some common examples are: (1) Blended family situations, which are near impossible to generalize; (2) Long-term relationships where partners choose not to get married but would prefer that their partner inherit their estate (Wisconsin law doesn’t recognize common law marriage); and (3) Early adulthood, where single young adults may prefer that their siblings, who may have young children, inherit instead of their parents, who may be empty nesters with a lifetime of retirement saving behind them.

Relying on intestate succession rules is just one reason to have a personalized estate plan created. Don’t leave your estate administration up to the state. Make your wishes known and protect your legacy with a clear estate plan unique to your family.

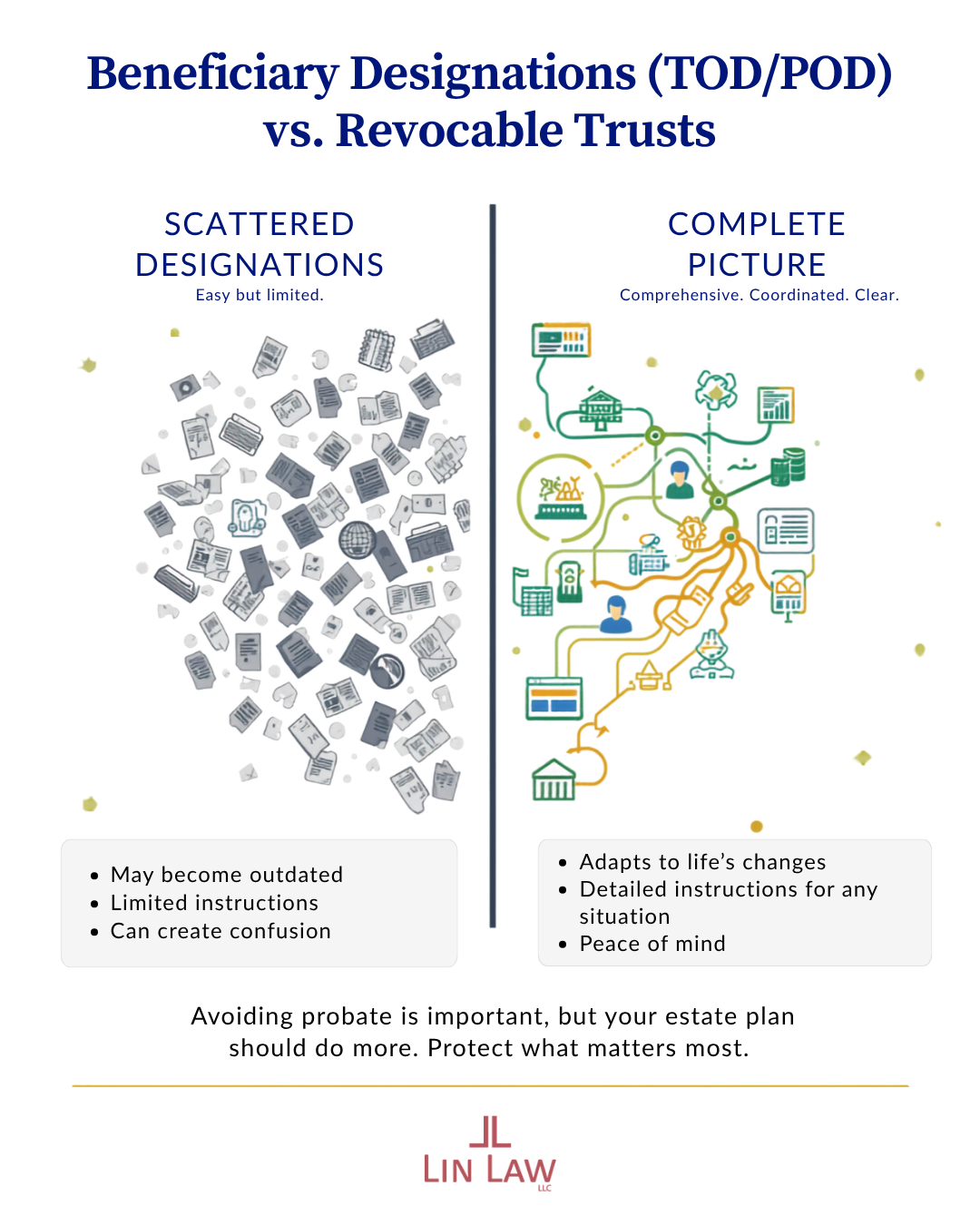

One of the most common misconceptions about estate planning is that adding beneficiary designations to your financial accounts will be enough to both avoid probate and have a comprehensive estate plan. However, while transfer-on-death (TOD) and payable-on-death (POD) designations can help pass assets directly to your heirs without probate, a clearly structured estate plan focuses on more efficiently managing assets and their distribution, since it takes into account unforeseen life changes that a TOD or POD designation does not account for. Avoiding probate alone should not be the only goal with respect to a complete estate plan.

One of the most common misconceptions about estate planning is that adding beneficiary designations to your financial accounts will be enough to both avoid probate and have a comprehensive estate plan. However, while transfer-on-death (TOD) and payable-on-death (POD) designations can help pass assets directly to your heirs without probate, a clearly structured estate plan focuses on more efficiently managing assets and their distribution, since it takes into account unforeseen life changes that a TOD or POD designation does not account for. Avoiding probate alone should not be the only goal with respect to a complete estate plan.

Persons involved in real estate closings and settlements are now required to report on certain transfers that the Treasury Department deems high risk for illicit financial activity. Specifically, non-financed transfers of residential real property to legal entities or trusts. The rule aims to in-crease transparency in real estate transactions and help prevent the use of anonymous entities to conceal illicit funds.

Persons involved in real estate closings and settlements are now required to report on certain transfers that the Treasury Department deems high risk for illicit financial activity. Specifically, non-financed transfers of residential real property to legal entities or trusts. The rule aims to in-crease transparency in real estate transactions and help prevent the use of anonymous entities to conceal illicit funds.

Did you know that Wisconsin is one of just nine states with marital (community) property laws? Wisconsin joined the small number of states with this treatment of marital property by enacting the Wisconsin Marital Property Act in 1986. Under Wisconsin’s marital property law, nearly all assets and debts acquired during a marriage are considered to be owned equally by both spouses, regardless of whose name is on the paycheck or whose name is on the title. The law is based on the principle that “a sound marriage is a partnership of equals,” recognizing the value of both financial and non-financial contributions to the relationship.

Did you know that Wisconsin is one of just nine states with marital (community) property laws? Wisconsin joined the small number of states with this treatment of marital property by enacting the Wisconsin Marital Property Act in 1986. Under Wisconsin’s marital property law, nearly all assets and debts acquired during a marriage are considered to be owned equally by both spouses, regardless of whose name is on the paycheck or whose name is on the title. The law is based on the principle that “a sound marriage is a partnership of equals,” recognizing the value of both financial and non-financial contributions to the relationship.

Even the best hitters can’t plan for every curveball life throws – but a strong estate plan, drafted by an experienced attorney familiar with your unique circumstances and goals, can bring your batting average up to all-star levels.

After Ted Williams passed away, confusion quickly ensued when two of his children presented a handwritten note expressing Mr. Williams’ desire that his body be cryogenically frozen. The problem? Mr. Williams’ will stated his wish to be cremated and have his ashes scattered over the ocean off the coast of Florida. The litigation that followed left Mr. Williams’ body frozen in controversy – like a batter getting thrown a 12-6 curveball.

Disputes like these can be avoided by properly documenting your wishes and by ensuring consistency across your estate planning documents. Wisconsin permits individuals to create Authorizations for Final Disposition – a special document that designates who will make burial or cremation decisions, and in which you may specify any specific funeral/celebration of life and burial arrangements.

At Lin Law LLC, we help families make sure their wishes are honored, their loved ones are protected, and their legacy is preserved.